LIBOR – THE DISHONORABLE RIDE INTO THE SUNSET

As the world contracts with technological advancements, awareness and transparency has become the mainstream, in almost all the spheres of life. The advancements, deferring to the theory of Butterfly Effect, exposed financial frauds and dubious accounting practices, that then gave way to reforms.

One such major scandal that was uncovered was the LIBOR rate manipulation by major international banks. London Inter-Bank Offered Rate, referred to as LIBOR, was the primary benchmark reference for short-term interest rates all around the world. It was an interest rate average that was derived from the estimates submitted by major international banks with the estimate indicating at what rate they were to transact with each other. However, given that those were estimates and not the actual rate at which they would transact, it was subject to manipulation which wasn’t unearthed till a decade back. Even with such unearthing, the LIBOR was only officially abandoned with effect from 2022.

SOFR – THE NEW KID IN THE BLOCK

Secured Overnight Financing Rate, referred to as SOFR, has been introduced as an alternative to LIBOR and is already in use for all the relevant financial contracts. It is administered by the New York Federal Reserve and overseen by the Alternative Reference Rates Committee (ARRC) which also publishes guidelines and best practice recommendations to standardize its use.

SOFR is a measure of the actual cost of borrowing/ lending overnight in the repo market. It is collateralized by US Treasury securities and is considered a risk-free rate. SOFR is calculated as a volume-weighted median of transaction level data on a particular business day and published on the next business day. It is published at 8 a.m. EST each day

Since, SOFR uses actual borrowing costs rather than estimates, it is considered less risky and less prone to manipulation like LIBOR.

SOFR – FEATURES

In the user guide, ARRC has listed the following as some of the characteristics of SOFR:

- It is derived from an active and well-defined market with sufficient depth to make it extraordinarily difficult to ever manipulate or influence.

- It is produced in a transparent, direct manner and is based on observable transactions, rather than being dependent on estimates, like LIBOR, or derived through models.

- It is derived from a market that was able to weather the global financial crisis and that the ARRC credibly believes will remain active enough in order that it can reliably be produced in a wide range of market conditions.

However, given that SOFR is an overnight rate, it is backward looking and not forward looking like LIBOR. As a result, ARRC has outlined various strategies to enable effective and accurate use of SOFR in contracts.

SOFR – TYPES

The following SOFR types are available for use in case of loans and other products:

SOFR

- Overnight rate published daily at 8 a.m. EST on the following day.

- Published by New York Federal Reserve.

- Backward-looking rate since it is based on actual borrowings.

- Choice between Simple vs Compound exists with additional options being In Advance vs In Arrears.

SOFR Averages

- Overnight rate published daily at 8 a.m. EST on the following day.

- Published by New York Federal Reserve.

SOFR Index

- Compounding sequence that allows investors to calculate compounded SOFR averages over custom time periods.

- Published by New York Federal Reserve every day after SOFR publication.

CME Term SOFR

- Daily set of forward-looking interest rate estimates, available for 1-month, 3-month, 6-month, and 12-month tenors.

- Published by CME Group Benchmark Administration Ltd.

- ARRC recommends limited usage only in support of business lending and the transition of legacy LIBOR cash products.

SOFR – DETAILED STUDY

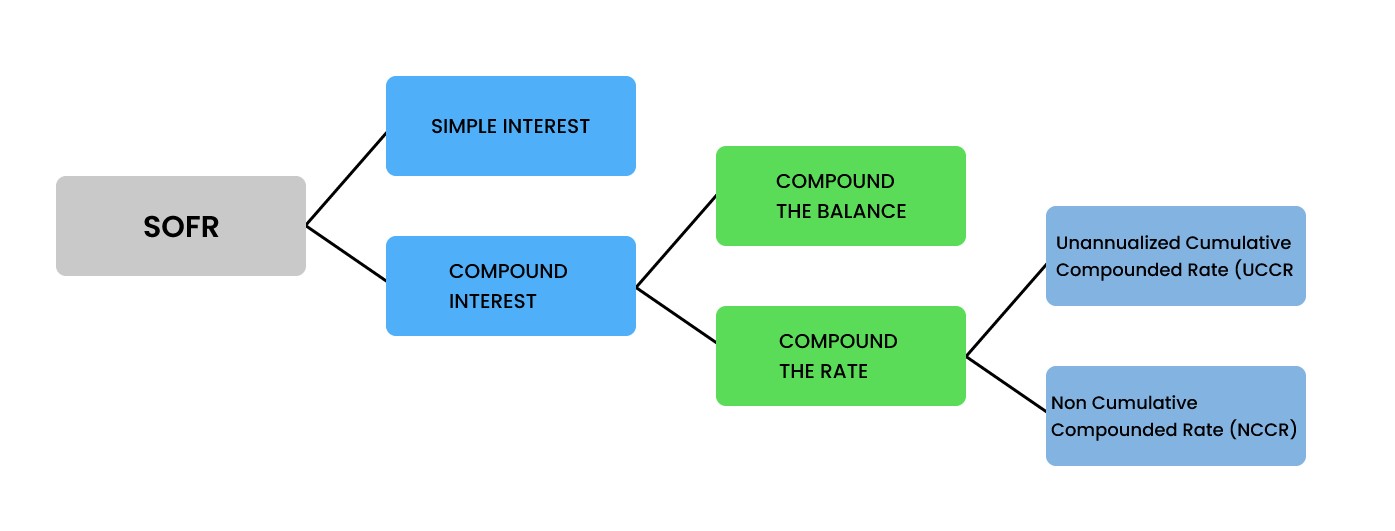

Simple vs Compound

Simple Interest

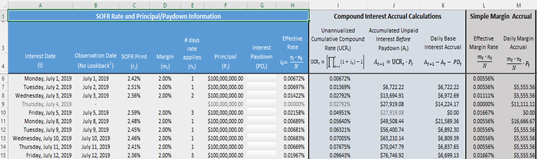

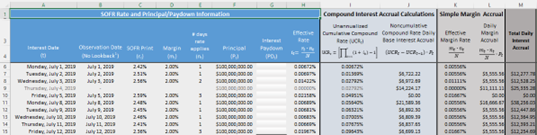

In the case of the Simple Interest method, the Daily SOFR is applied on the outstanding principal of the loan. Daily Simple SOFR and SOFR Average will technically give the same result at the end of the interest period, as long as no principal repayment is made during the interest period.

Compound Interest

In the case of the Compound Interest method, the Daily SOFR is compounded daily and applied on the outstanding principal of the loan. There are 2 methods to arrive at the compound interest, explained below:

Compound the Balance

In this method, the Daily SOFR is applied on the opening balance which is comprised of outstanding principal and unpaid accrued SOFR interest till that date. This method can be applied regardless of whether principal repayments are made or whether some portion of interest is repaid during the interest period.

Compound the Rate

This method compounds the rate itself and can be applied only under specific conditions:

- Principal remains constant during the interest period.

- If principal is repaid, a proportionate amount of accrued interest is also repaid along with the same.

Cumulative Compounded Rate (CCR)

This method involves calculation of a single cumulative compounded rate using which interest can be calculated for the entire interest period.

Non-Cumulative Compounded Rate (NCCR)

NCCR is derived from the CCR i.e., CCR of the current day minus CCR of the previous day. This method uses the compounded rate so derived and facilitates calculation of a daily interest accrual amount. As a result, this method calculates the accurate periodic interest at any point in time.

NCCR is the method recommended by ARRC since it supports intra-period events like prepayments.

Notice of Payment

In Advance

SOFR in advance uses interest rates that have been derived from previous periods. This method is helpful since the interest amount is certain and would be known at the start of the interest period. This is however not a preferred method since it is based on past averages and does not always reflect the current reality.

In Arrears

SOFR in arrears can be Daily Simple SOFR in arrears and Daily Compounded SOFR in arrears. This method uses the daily SOFR published, during the interest period. This remains the preferred method since it is near accurate though the interest amount is not known at the start of the interest period.

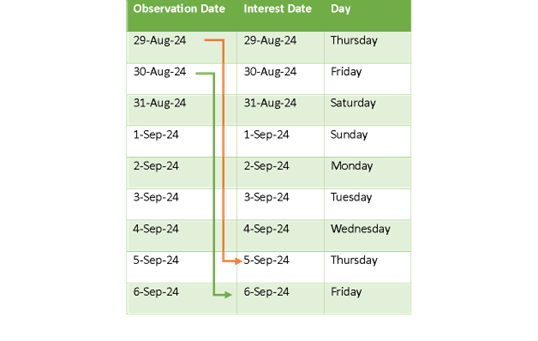

Lookback Period and Observation Shift

One of the recommended conventions is to include a lookback period which allows sufficient notice of the final interest payment in case of ‘in arrears’ method. Such lookbacks included further conventions like with observation shift, without observation shift etc.

Lookback method involves deriving the rates of the Observation period that mirrors the Interest period with the lookback days acting as the interval days. To put it simply, Interest Date is the date for which interest is calculated while the interest rate used is based on the corresponding Observation Date. While Simple Interest method does not differentiate between calendar days & business days, Compound Interest method demands lookback days to be business days.

For example, with a lookback of 5 business days, Interest on 5-Sep-2024 would be calculated based on the rate of 29-Aug-2024 since 31-Aug-24 and 1-Sep-24 are weekend holidays i.e., non-business days. Apart from weekend holidays, other holidays as published in the New York Federal Reserve website are also excluded since they are non-business days.

HOW CAN KUBER TMS™ HELP YOU MANAGE YOUR SOFR NEEDS?

Our product Kuber TMS™ with a sophisticated and user-friendly interface adequately supports the creation and management of business loan products which are referenced by SOFR. Our software allows the interface of rates on a daily basis which will then be automatically applied to the relevant loans.

Kuber TMS™ covers the following aspects of SOFR loan management:

- Creation of SOFR benchmark records and daily interface of published rates which automatically updates rates/ recalculates interest amounts in the linked loans.

- Ability to record preferred rounding precision and holiday calendar for the required periods at the benchmark record level.

- Ability to define lookback period at the benchmark record level.

- Ability to record drawdowns from the Child Facility as individual Loan records referencing the SOFR benchmark.

- Ability to record loan details like BS Classification/ Type/ Duration Classification that can then be harnessed for reporting purposes.

- Ability to record processing fees that are to be amortized in line with IFRS 9 requirements or fees/ charges that are to be expensed, along with the tax details.

- Ability to create and apply principal repayments like scheduled repayments, bullet/ balloon repayments etc.

- Ability to value Forex loans on a regular basis for calculation of unrealized forex gain/ loss.

- Ability to review and approve settlement lines for configurable host-to-host transmission.

- Generation of relevant accounting entries in draft status enabled for transfer to ERP GL.

- Availability of standard out-of-the-box reports as well as custom reports covering all aspects of loan management.

- Availability of Dashboards covering all aspects of loan management.

In addition, Kuber TMS™ provides the following standard features:

- Master Management

- Dynamic alerts and notifications in software as well as through email

- Role Management and access control based on Create, Read, Update, Delete (CRUD) model

- Approval Management involving configurable approval rules and multi-level approval workflow

- Integration with third-party websites for import of exchange rates

These are only some of the numerous products/features available in Kuber TMS™. For a personalized consultation and to discover how Kuber TMS™ can customize and automate your treasury operations seamlessly:

Visit us at kubertms.com